Introduction

Numeracy is a key skill that supports all aspects of financial literacy, enabling individuals to manage their finances effectively and make informed decisions. Finances and numeracy are closely intertwined, and several key issues revolve around their intersection. Enhancing numeracy skills and promoting financial education are critical steps in addressing these key issues, empowering individuals to make informed financial choices and secure their financial well-being.

Key Issues

At the intersection of finances and numeracy are the following key issues:

- Financial Literacy: A lack of numeracy can hinder financial literacy, making it difficult for individuals to comprehend financial concepts and make informed decisions.

Budgeting: Managing personal finances requires strong numeracy skills to create and stick to a budget, track expenses, and set financial goals effectively.

Consumer Choices: Numeracy influences decisions when comparing prices, calculating discounts, and evaluating the value of purchases.

Taxes: Understanding tax calculations, deductions, and credits is essential to optimize one’s financial situation and avoid costly errors.

Debt Management: Numeracy is crucial for understanding interest rates, loan terms, and debt repayment strategies, preventing individuals from falling into financial traps.

Financial Security: Inadequate numeracy can leave individuals vulnerable to financial scams and fraud, as they may struggle to recognize deceptive financial schemes.

Retirement Planning: Planning for retirement necessitates numeracy to estimate future income needs, assess pension options, and determine savings goals.

Economic Disparities: Numeracy disparities can exacerbate income inequalities, limiting financial opportunities for those with lower numeracy skills.

Economic Mobility: Numeracy skills play a pivotal role in an individual’s ability to improve their financial situation and achieve upward economic mobility.

Investment Decisions: Making informed investment choices demands numeracy skills to assess risk, calculate returns, and diversify portfolios wisely.

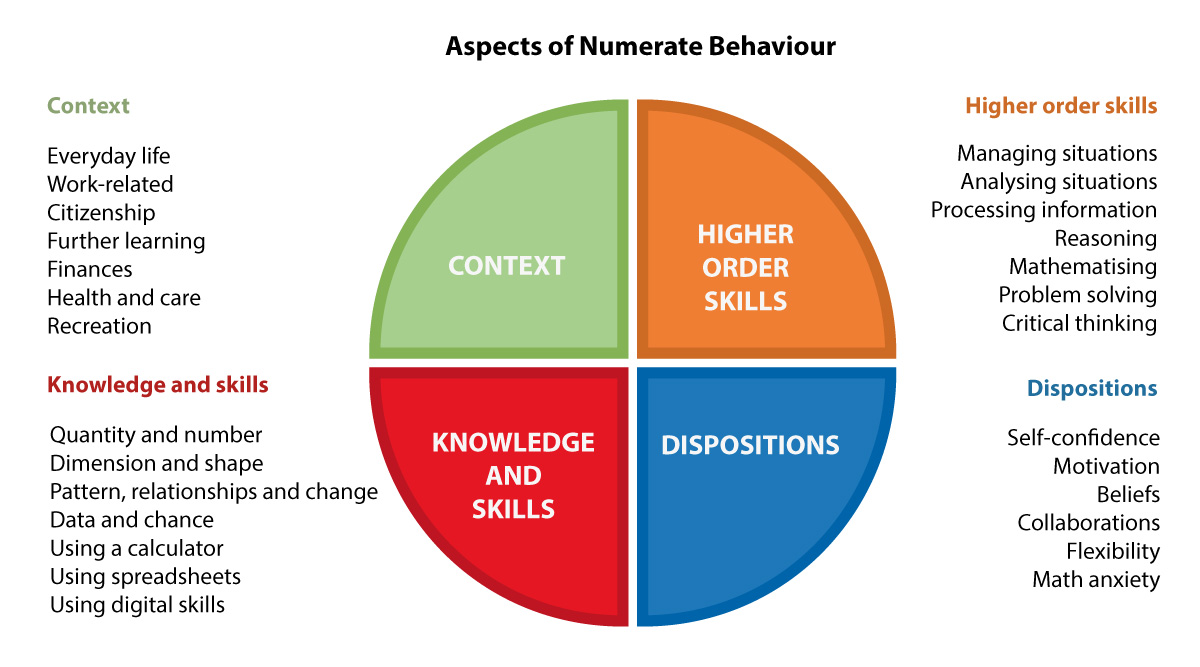

In managing situations, higher-order skills play an essential role.

The quality of the mathematical action depends on how the person relates himself to his or her mathematical knowledge and skills (dispositions) and the extent to which he/she can oversee and control a situation (higher-order skills).

Relation to Framework

Suggestions for PD meetings

Discussing personal experiences

Set up a group discussion on personal experiences. Discuss personal experiences with some selected aspects of financial activities in daily life. Make explicit when and which numeracy issues are involved when dealing with financial matters.

Financial choices

Discuss the flowing issue around numeracy and financial literacy.

In recent years, the financial world has become more complex and intricate. In this context, numeracy and, particularly, financial literacy, are seen as paramount in providing consumers with the knowledge and confidence required to take part in financial markets. Despite some indicative empirical findings, it is still to be ascertained how the two competences differentially contribute to the quality of decision-making in financial contexts. Furthermore, it is still unknown to what degree financial literacy and numeracy, taken as relevant mind-ware for financial decision-making, are effective in guarding against well-documented biases such as loss aversion and framing effects. This study aims to clarify these issues by employing an experimental task, conceived as an approximation to real-world decision-making involving the sale of shares. Our results suggest that numeracy and financial literacy affect decision-making differently in a pattern that, in part, runs counter to conventional economic theory. The data indicate that numeracy promotes a pattern of choices closer to economic rationality, while financial literacy can prove counterproductive and may amplify cognitive biases, namely framing effects and loss aversion. The outcomes are interpreted in light of dual-process theories, and the political implications discussed.

Moreira Costa, V., de Sá Teixeira, N. A., Cordeiro Santos, A., & Santos, E. (2021). When more is less in financial decision-making: financial literacy magnifies framing effects. Psychological Research, 85(5), 2036–2046. https://doi.org/10.1007/s00426-020-01372-7

Advertisement on borrowing money

Collect advertisements for borrowing money. Discuss in small groups what are the key elements to look at in the advertisements.

Activity: Think, Pair, Share.

Background information

There are a lot of tests to assess financial competencies, also in relation to numeracy. However, most of them focus on rather sophistication knowledge on financial products, like stocks. The mathematical part of these tests in many cases are only focusing on rote calculations often with fractions.

There are no tests yet which encompass also the higher order skills, as they are mentioned in the CENF. YThisn is still an under-researched area, notwithstanding the common sense idea that dispositions will affect financial decision-making.

For insight in some tests see: Storozuk, A., & Maloney, E. A. (2023). What’s Math Got to Do with It?: Establishing Nuanced Relations between Math Anxiety, Financial Anxiety, and Financial Literacy. Journal of Risk and Financial Management, 16(4), 238. https://doi.org/10.3390/jrfm16040238

Literature

Darriet, E., Guille, M., Vergnaud, J. C., & Shimizu, M. (2020). Money illusion, financial literacy and numeracy: Experimental evidence. Journal of Economic Psychology, 76. https://doi.org/10.1016/j.joep.2019.102211

Moreira Costa, V., de Sá Teixeira, N. A., Cordeiro Santos, A., & Santos, E. (2021). When more is less in financial decision-making: financial literacy magnifies framing effects. Psychological Research, 85(5), 2036–2046. https://doi.org/10.1007/s00426-020-01372-7

Leumann, S. (2017). Representing Swiss vocational education and training teachers’ domain-specific conceptions of financial literacy using concept maps. Citizenship, Social and Economics Education, 16(1), 19–38. https://doi.org/10.1177/2047173416689687

Moreira Costa, V., de Sá Teixeira, N. A., Cordeiro Santos, A., & Santos, E. (2021). When more is less in financial decision-making: financial literacy magnifies framing effects. Psychological Research, 85(5), 2036–2046. https://doi.org/10.1007/s00426-020-01372-7

OECD. (2013). PISA 2015 assessment and analytical framework: Mathematics, reading, science, problem solving and financial literacy. OECD Publishing: http://dx.doi.org/10.1787/9789264190511-en

Peters, E., Tompkins, M. K., Knoll, M. A. Z., Ardoin, S. P., Shoots-Reinhard, B., & Meara, A. S. (2019). Despite high objective numeracy, lower numeric confidence relates to worse financial and medical outcomes. Proceedings of the National Academy of Sciences, 116(39), 19386–19391. https://doi.org/10.1073/pnas.1903126116

Peters, E., & Shoots-Reinhard, B. (2023). Better decision making through objective numeracy and numeric self-efficacy. In Advances in Experimental Social Psychology (pp. 1–75). Academic Press Inc. https://doi.org/10.1016/bs.aesp.2023.03.002

Skagerlund, K., Lind, T., Strömbäck, C., Tinghög, G., & Västfjäll, D. (2018). Financial literacy and the role of numeracy – How individuals’ attitude and affinity with numbers influence financial literacy. Journal of Behavioral and Experimental Economics, 74(August 2017), 18–25. https://doi.org/10.1016/j.socec.2018.03.004

Storozuk, A., & Maloney, E. A. (2023). What’s Math Got to Do with It?: Establishing Nuanced Relations between Math Anxiety, Financial Anxiety, and Financial Literacy. Journal of Risk and Financial Management, 16(4), 238. https://doi.org/10.3390/jrfm16040238

Sunderaraman, P., Barker, M., Chapman, S., & Cosentino, S. (2022). Assessing numerical reasoning provides insight into financial literacy. Applied Neuropsychology: Adult, 29(4), 710–717. https://doi.org/10.1080/23279095.2020.1805745

van Campenhout, G. (2015). Revaluing the Role of Parents as Financial Socialization Agents in Youth Financial Literacy Programs. Journal of Consumer Affairs, 49(1), 186–222. https://doi.org/10.1111/joca.12064

Systematic reviews

Lusardi, A., & Mitchell, O. S. (2011). Financial literacy around the world: an overview. Journal of Pension Economics & Finance, 10(4), 497–508. https://doi.org/10.1017/S1474747211000448